Best Trends Shaping Digital Payments will be discussed in this article. The method of payment used by consumers is quickly changing. Credit and debit cards seem like a thing of the past as a result of the growth of digital payments. Yet (for the time being), they continue to rule the payment industry. Deferred payment plans, contactless payments, and ongoing digitization have all grown in popularity during the past few years. Will anything of the above change in 2023? Here are six payment trends that can help us anticipate what this year will bring.

Top 6 Trends Shaping Digital Payments In 2023

In this article, you can know about Digital Payments here are the details below;

1. BNPL Adoption continues to Grow

It’s not exactly a novel concept to purchase a goods first and then pay for it later. However, it has recently experienced a significant rebirth, particularly with the increase in online purchasing brought on by the pandemic. The world’s fastest-growing eCommerce payment method right now is Buy Now Pay Later (BNPL). Insider Intelligence estimates that by 2022, one in three American consumers will have utilized a BNPL program in some capacity. 41% of people, according to Fool.com, claim to have utilized a BNPL service to save money for a crisis. Another 25% of people utilize it as a result of income loss. BNPL purchases already account for 1% of all US retail eCommerce expenditure, which is a far larger percentage than it might first appear.

According to Hans Zandhuis, president of Ally Lending, the typical BNPL purchase costs about $200. And even this growth had been accelerating for some time, it skyrocketed by 2021. More than half of all consumers polled by the Motley Fool’s Ascent service in March 2021 reported using a BNPL service. That contrasts with a third about the halfway point of 2020. This makes sense given that American consumers are now more aware of how BNPL services operate. Strongholds in eCommerce like Amazon and Wal-Mart have offered options for delayed payment in response.

Although several generations have adopted the BNPL payment method, it is primarily used by millennials and generation Z, who weren’t reared with conventional credit cards. By 2025, $1 trillion in global Buy Now, Pay Later expenditure is expected, according to CBInsights. For comparison, the annual amount of all US spending is roughly $8 trillion. Worldpay, a company that processes payments, predicts that BNPL sales would reach $166 billion yearly in 2023. That would make up about 5% of international eCommerce outside of China.

These services aren’t just grabbing users’ attention. Five major BNPL providers—Affirm, Afterpay, Klarna, PayPal, and Zip—are being questioned in-depth by the Consumer Financial Protection Bureau about their operations, goods, and compliance with consumer protection legislation. A BNPL service has been used by more than 40% of Americans. 38% of them have missed at least one payment, and for 75% of them, doing so has had a negative effect on their credit score. In addition, a March 2021 study revealed that 53% of respondents who had never utilized a BNPL service were at least somewhat inclined to do so the following year. Although PayPal continues to be the most popular option, Klarna was the first Buy Now, Pay Later service. With 361 million active users as of August 2021, PayPal has a sizable customer base to which they can currently provide the service.

2. Contactless Payments and Tap-To-Mobile Technology Are Changing Retail

More customers than ever before tap their cards and phones at checkouts, even in remote locations. The icon that indicates a card reader supports tap payments is one that everyone is accustomed to seeing. Furthermore, this trend is being accelerated by the COVID-19 Pandemic. A Visa poll found that almost 50% of consumers believe contactless payments are one of the most crucial safety measures currently available in a retail establishment. Also check Hacks To Go Viral On TikTok For Businesses

Additionally, more than 50 percent of millennial consumers stated they would avoid a retailer if it didn’t provide a contactless option. The statistics have shown this as well. In the first half of 2020, Visa contactless card usage increased by around 150%. Additionally, the number of mobile users making payments is anticipated to rise year over year, reaching 114.8 million in 2023. What about small business owners that lack POS systems? Using a contactless card or mobile wallet, customers will be able to transmit a payment immediately through the merchant’s phone thanks to tap-to-mobile technology. According to experts, Tap-to-Mobile will finally become a reality in 2022, boosting revenues for small enterprises.

Companies like Mastercard and Visa, who launched programs dubbed Tap on Phone and Tap to Phone, respectively, are already implementing it. On its platform, tap-to-mobile transactions actually increased by 30% in 2021, according to a report from Visa. A mobile point-of-sale terminal can be any mobile device with an NFC chip. By 2026, 32 million of these mPOS terminals are anticipated to have been shipped. With 87.3% of smartphone users in China making payments via mobile proximity in 2021, China is the world leader in this field.

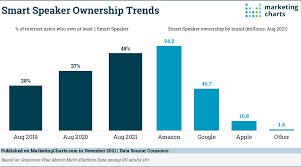

3. More people are Paying Through Smart Speakers

Voice-activated payments and money transfers are becoming more and more popular among users of smart speakers and other similar devices. Over 120 million smart speakers are thought to be in use in the United States today. In contrast, there were only 20 million in 2017. But even in 2017, 28% of smart speaker owners used voice commands to send money and complete transactions. The number of individuals using their smart speakers to make payments is only going to increase as more and more people continue to use them to buy. According to a poll by PwC, in 2021, 50% of voice assistant users will use their device to make a transaction.

Of those, 40% make monthly purchases using their smart speaker. 10% of people do it every day. The total amount of transactions made through smart speakers is currently $4.6 billion. In 2023, this amount is projected to more than quadruple to $19.4 billion. Therefore, it makes sense that Business Insider estimated that by the end of 2022, the 18.4 million users who made payments via their smart speakers in 2017 would increase to 77.9 million. Despite the fact that many users worry about the security of voice assistant payments, this is all the case.

According to a recent PaySafe Group study, 33% of people are uncomfortable utilizing voice commands to make payments. According to the research, voice commands are most comfortable when used to make minor payments, like those for groceries or public transit. Unsurprisingly, expensive items like furniture and vacation packages are near the bottom of the list. Despite users’ reluctance, some businesses are moving toward greater voice payments due to the security offered by biometrics.

4. More Business, services, and products use embedded payments

The development of delivery apps, carpool services, and omnichannel retail have shown us that consumers value convenience. This contributes to the explanation of why embedded payments have spread so widely. undefinedOver the previous five years, searches for the term “Embedded Payment” have increased by 433%.

Payments that are included into a service or good are called embedded payments. Typically, they are digital services or goods (think of websites, eCommerce stores, mobile applications, and ride-sharing apps), but this is not a must (consider eating establishments, Teslas, etc.). Embedded payments are also becoming more and more important because approximately half of all retail sales are now made online. Therefore, it should come as no surprise that almost half of the merchants surveyed in a recent Omdia study stated that enhancing integration with their payment gateway would be the most efficient strategy to lower friction in digital payments.

In 2020, the market as a whole earned about $22 billion in revenue. However, it is anticipated to expand more quickly than the majority of other payment and fintech sectors.By 2025, the embedded finance sector is expected to generate around $230 billion in revenue, according to Statista. PYMNTS.com predicts that the embedded banking sector will be worth $7 trillion by 2031, which is even more remarkable. Embedded payments are altering how consumers make purchases even outside of the high-tech innovation environment.

Consider Starbucks as an example. The coffee juggernaut reported that more than 25% of total sales came from mobile orders as of the second quarter of 2021. Actually, the Starbucks app is currently the second-most popular proximity mobile payment app in the United States. Embedding payment choices in a digital space, such as a smartphone app, is the future of embedded payments in the majority of scenarios.

5. Digital Wallets continue to Increases in Popularity

A person once wouldn’t have thought to leave the house without their wallet. People now purposefully engage in that behavior. 15% of people who use digital wallets don’t even bother to take their physical wallets with them when they leave the house, according to McKinsey & Co. If they aren’t planning to buy anything, another 11% think of leaving their wallets at home. The majority of users load several cards into their digital wallets. 40% of people with multiple payment options loaded alternate between cards every few weeks. Card issuers have been urging customers to add their cards to their mobile wallets because they want to be at the head of that heap.

The majority of customers change payment cards based on which cards have available funds, but many do so because they prefer to use particular cards for particular transactions. Others use various cards in accordance with the discounts and promotions that the card providers provide. 46% of consumers will use digital wallets in 2020. This percentage was only 18.9% in 2018. Payments made with digital wallets will reach $10 trillion by 2025, nearly double the $5.5 trillion in payments made in 2020, predicts Juniper Research. Expect to see a significant increase in the use of biometric authentication to protect digital wallets in the near future.

6. Peer-to-Peer Payments are expected to takeoff

Peer-to-peer (P2P) payments have grown to be a significant component of the digital payments ecosystem, despite the fact that merchants aren’t always involved. Users can easily transfer money among each other using these apps, which are almost all mobile apps. Understanding current usage statistics for all P2P systems is challenging. However, eMarketer predicted that by 2021, the top three providers (Zelle, Venmo, and Square’s Cash App) would have a combined user base of 165.7 million. That represents about 50% of all Americans.

Additionally, according to eMarketer, the P2P sector will produce more than $1 trillion in transaction volume by 2023 (up from $785.9 billion at now). The top three players, as mentioned above, are responsible for this type of growth. For the following four years, Venmo, the largest of the three, is anticipated to increase by more than 50% yearly. The first of the three major services, Venmo was established in 2009. It was bought by Paypal in 2012 for $800 million, and it has remained at the top ever since. Venmo has historically emphasized the social side of P2P payments, attracting and keeping the most users over the course of its existence.

On the other side, a group of banks came together to launch Zelle. Users must connect a Visa or Mastercard linked to a supported bank account because it has a higher end market focus. In 2020, the average transaction value on Zelle exceeded $270. Contrarily, the typical transaction value on Venmo is about $60. The higher transaction volume has historically led to Zelle processing more transactions than its rivals. It processed more than $300 billion in 2020. By the end of 2022, it was anticipated to handle over $500 billion. By comparison, Venmo is predicted to generate $304 billion by the end of 2023.

In general, it is anticipated that Venmo’s user base will expand more quickly than Zelle’s. However, it is still expected to expand at a strong 30%+ annual rate. The incoming Gen Z generation of users is anticipated to be largely responsible for this growth. Just over a third of Gen Z users currently utilize a P2P payment app. However, it’s anticipated that by 2025, nearly two-thirds of the Gen Z cohort would be utilizing a P2P payment app.

Conclusion

In general, the payments sector is evolving quickly. Consumer requirements are coming to the fore as the digital and physical worlds merge. The payments sector is continually changing to accommodate how consumers shop, whether it’s accepting alternative forms of payment, offering credit for modest purchases at the register, or sending money to pals.